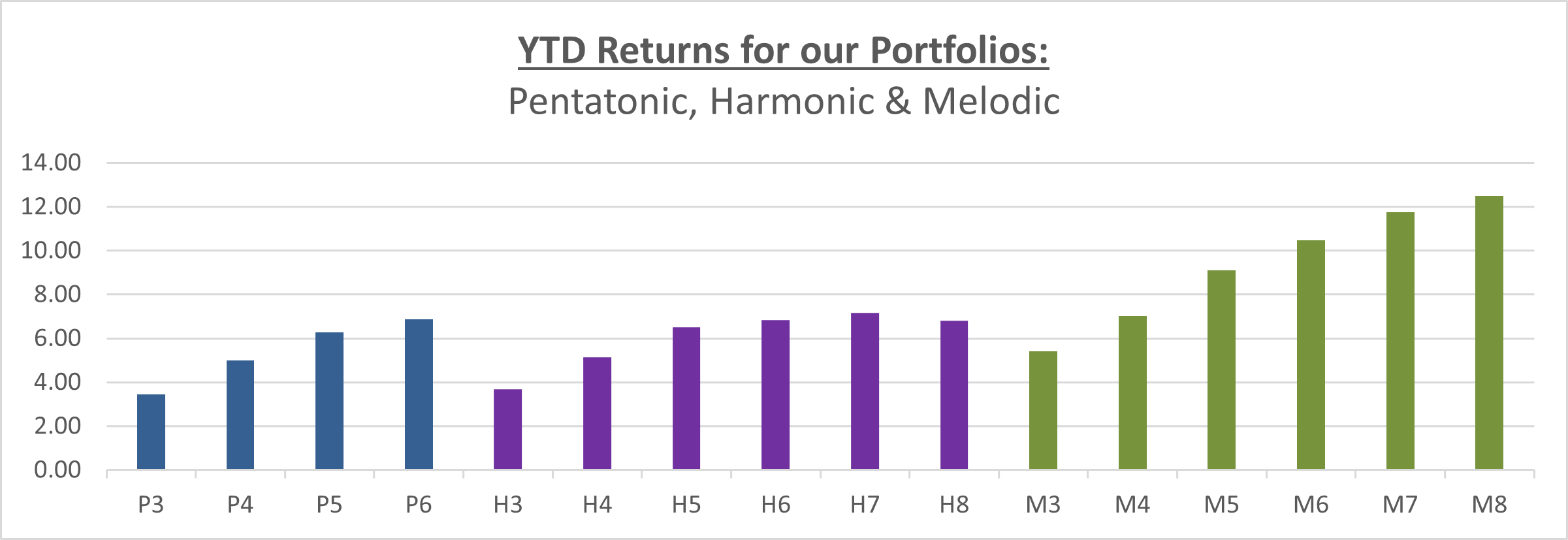

Model Portfolios have all shown a positive return since January 1st as the following table shows. The returns per portfolio are an indication only and are to identify the growth per level of risk within each portfolio range.

(Click chart to open a larger version in a new window)

I have reduced the portfolio return by the maximum ongoing fee a client could pay (except Offshore Bond investors). The figures for the Pentatonic Income Portfolio assume income is reinvested as I am unable to strip out the dividend that has been paid.

The Harmonic (H) Portfolios have more exposure to Emerging Markets as the targeted level of risk increases. With Emerging Markets having had a sell off recently – the higher the level of risk, the more exposure they have and as a result, they have been affected more.

The Melodic Portfolios are Socially Responsible Investments (SRI) and have not suffered the same drop recently, because of their reduced exposure to Emerging Markets and Global Bonds. Both of these areas should recover and therefore the gap between the SRI and unconstrained portfolios will reduce.

Market summary 3rd Quarter 2021

In summary, we saw a slightly less profitable quarter compared to Q2. The impact of Covid 19 is still noticeable across certain sectors and as we write this report, the World is suffering with the uncertainty over the new Covid mutation.

Here are some observations of a few areas we invest in.

UK

Overall UK Equities rose in Q3 despite some noticeable dips in performance because of supply chain issues and fuel shortages. The microchip shortage had a major impact on production and indeed overall GDP figures. Bearing in mind you find microchips in any product you buy with a screen, from a hoover through to a new car, a shortage of production in the Far East has had a knock-on effect in the UK and the rest of Europe.

Fuel shortages also had a part to play in the small dips in the market. Luckily it wasn’t an issue with the supply of fuel itself and was to do with the lack of professional drivers to deliver the fuel and was soon rectified across the markets.

There were some clear sector winners in Q3. Low value grocery retailers saw good performance throughout Q3 as did the Mergers and Acquisition markets driven by the bid activity for Wm Morrisons acquisition and a proposal from an American sports betting group to purchase UK owned Entain.

There were also some big bids being made for aerospace and defence equipment manufacturing companies.

US

US equities saw a small positive return at the end of Q3. This was because of strong earnings and a bearish approach from the FED around raising interest rates and the tightening of quantitative easing. It is anticipated that the FED will start to announce their plans to do both by the end of 2021.

On a sector basis, financials and utilities performed well and industrials and material supplies were the worst, with the exception of energy. Energy prices in the US rose the same as the rest of the world due to supply demands.

Emerging Markets

Emerging markets equities fell during the 3rd quarter due to concerns around supply chain disruptions continuing and worries over higher food prices and energy supplies. This led a sell-off in the Chinese stock market.

The concerns around supply chain disruptions were further compounded due to some Covid-19 restrictions being re-introduced and the collapse of Evergrande which created a worry around the potential for systematic financial system risk.

Brazil were the weakest market in Q3 off the back of being the best performing market in Q2. South Korea also reported losses throughout Q3 amid concerns around the falling prices of microchips.

By contrast energy exporters outperformed in Q3 most notably Colombia, Russia and the Middle East.

India is now back on track to deliver at least one vaccination to 70% of its population which helped India’s economy to recover too.

Summary

We are not recommending any changes to the Portfolios this quarter as we believe the current asset spread and fund choice provides an excellent spread of exposure.

The information provided in this report is based on our own opinion and offers no guarantee that expectations will be met. Past performance is no guide to future results. As always, should you have any concerns you wish to raise, please do contact us.

Keep safe